Table of Contents

A price target is not the whole story

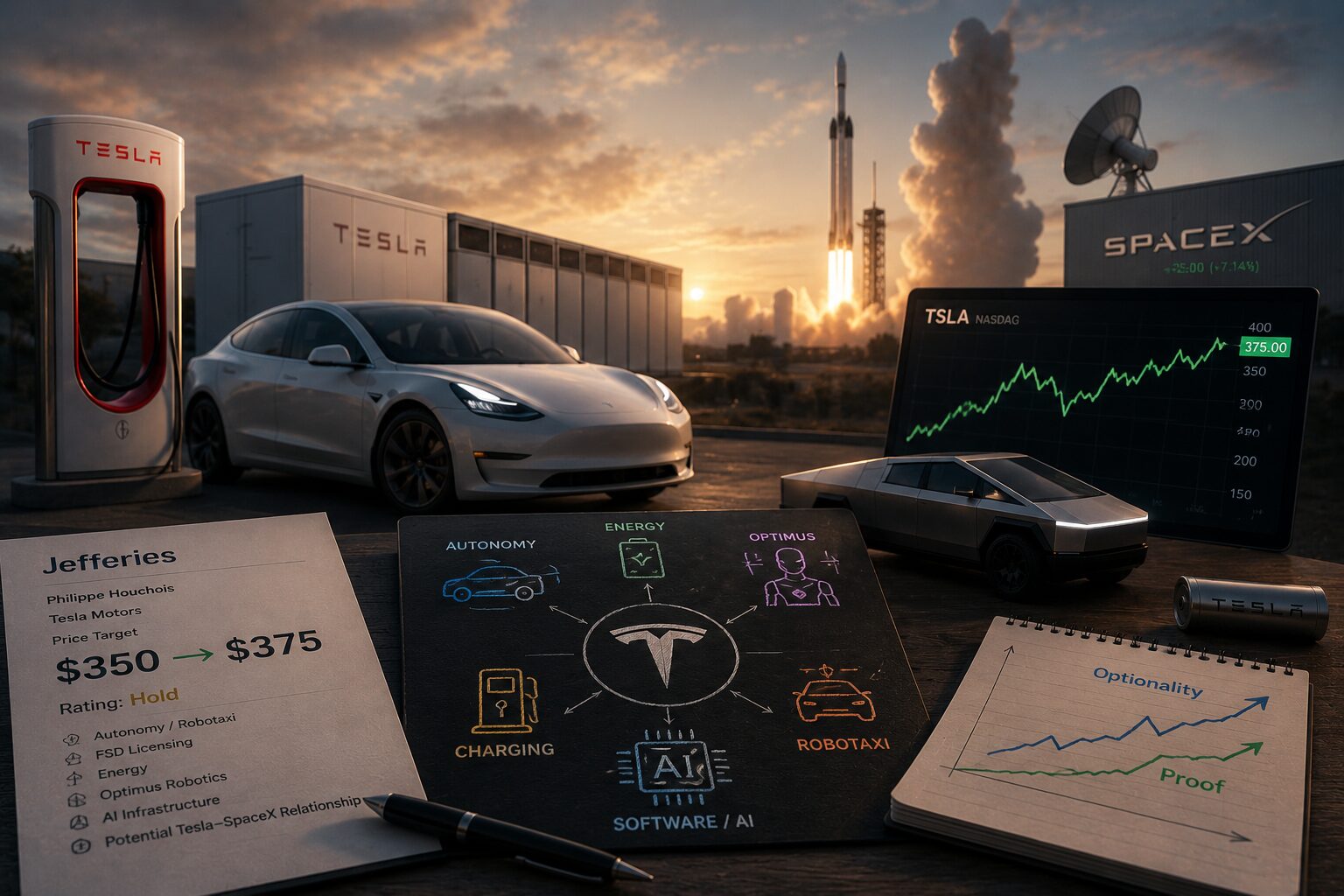

A post from Ming said Jefferies analyst Philippe Houchois raised Tesla’s price target from $350 to $375 while keeping a Hold rating. The post also framed the update around several future-facing drivers, including the idea that investors are talking more about a closer Tesla-SpaceX relationship.

One analyst note is not destiny. Price targets move all the time, and a Hold rating is not exactly a loud endorsement. The more interesting point is what the market is being asked to value when it values Tesla.

For a traditional automaker, valuation usually starts with units, margins, inventory, incentives, factories, and the product cycle. Those still matter for Tesla. But Tesla’s equity story now also includes robotaxis, possible FSD licensing, Optimus, energy storage, AI infrastructure, charging, software, and the orbit of Elon Musk’s other companies. That makes the stock unusually sensitive to new narratives.

Tesla is being valued like a portfolio of options

Tesla bulls often treat the company as a portfolio of call options. The auto business funds the platform. Energy storage adds another industrial growth engine. FSD and robotaxis could create high-margin software or mobility revenue. Optimus could open a robotics market. Charging could become infrastructure. AI training could become an internal advantage.

The bear case is that this framing can excuse weak near-term fundamentals. If vehicle margins fall, bulls can point to autonomy. If robotaxi timelines slip, they can point to energy. If energy runs into capacity limits, they can point to Optimus. That flexibility can be a strength or a trap, depending on execution.

The reported Jefferies target increase sits inside that tension. A higher target with a Hold rating suggests some room for future value, but not enough conviction to ignore the risks. That is probably where many professional investors are: Tesla is too unusual to value like GM, but too uncertain to value purely like an AI platform.

Why SpaceX keeps entering the conversation

The idea of a Tesla-SpaceX merger, partnership, or closer strategic combination comes up often in online Tesla circles. It is easy to see why. Both companies share Elon Musk and a taste for vertical integration, manufacturing intensity, software-heavy engineering, and big infrastructure bets. Tesla builds vehicles, batteries, autonomy, energy systems, and robotics. SpaceX builds rockets, satellites, communications networks, and space logistics.

Investors still need to separate imagination from probability. A merger would be complicated. Tesla is public; SpaceX is private. Their capital needs, regulatory exposure, investor bases, and business models are different. Any formal combination would raise governance, valuation, and strategy questions.

Even without a merger, SpaceX affects how some investors see Tesla. It reinforces the idea that Musk-led companies can enter difficult physical industries and change cost curves. It also encourages a broader Musk ecosystem view, where AI, manufacturing, energy, autonomy, communications, and robotics might eventually overlap.

That perception can support Tesla’s multiple. It can also make the stock harder to anchor.

The risk is narrative overload

Tesla’s biggest investor advantage may also be one of its biggest risks: the company always has another story. When the market is optimistic, Tesla can look like a bundle of future monopolies. When confidence weakens, the stock can look detached from results that are already visible.

Narrative overload matters because each future business needs different proof. Robotaxis require safety performance, regulatory approval, fleet economics, and consumer trust. Optimus needs durable hardware, useful autonomy, lower manufacturing cost, and real deployment. Energy storage needs capacity, project execution, grid demand, and margins. Vehicle growth still needs attractive models at competitive prices.

Bundling all of that into one valuation is tempting. It can also hide the weak links.

What investors should watch instead

A practical way to analyze Tesla is to separate optionality from proof. Optionality means a business could become valuable. Proof means it is already showing measurable financial or operating traction.

For autonomy, watch miles, interventions, regulatory permissions, paid adoption, and insurance or safety signals. For robotaxi, watch fleet size, service area expansion, utilization, cost per mile, and incident transparency. For Optimus, watch factory deployment, useful tasks, and production cost. For energy, watch Megapack deployments, backlog, margins, and grid-service demand. For vehicles, watch price stability, delivery growth, refresh cadence, and regional competitiveness.

That approach makes the valuation debate less emotional. Tesla does not need every future business to work to justify a premium. But the premium becomes fragile if too many promises stay in demo mode.

The reported Jefferies target increase captures the moment well. Tesla is not being valued only as a car company, but it still has to prove enough real businesses to support the market’s expectations. SpaceX speculation, AI ambition, and robotaxi excitement can lift imagination. Execution is what keeps imagination from turning into air.

Source

- Ming X post on Jefferies raising Tesla price target to $375 and related outlook points: https://x.com/tslaming/status/2068931579599376586

- Tesla Investor Relations: https://ir.tesla.com/

- Tesla AI page: https://www.tesla.com/AI

- Tesla Energy page: https://www.tesla.com/energy

- Tesla Robotaxi page: https://www.tesla.com/robotaxi

- X trending page included by user: https://x.com/i/trending/2069446940035514742?timeline=VGltZWxpbmU6CgCaHLgnBw5WAXYA